As featured on ABC, CBS, NBC, & FOX TV, U.S. News & World Report, USA Today, FEDweek, GoBankingRates, yahoo!finance, AOL Finance, MSN money, Nasdaq Personal Finance & more.

Federal Solutions

Contributing to the National Conversation

By: Eric Steffy, Federal Solutions Support

Published in FEDweek: April 9, 2026

While federal agencies automatically contribute 1% of pay regardless of participation, contributing at least 5% allows employees to receive the full government match, essentially doubling their savings.

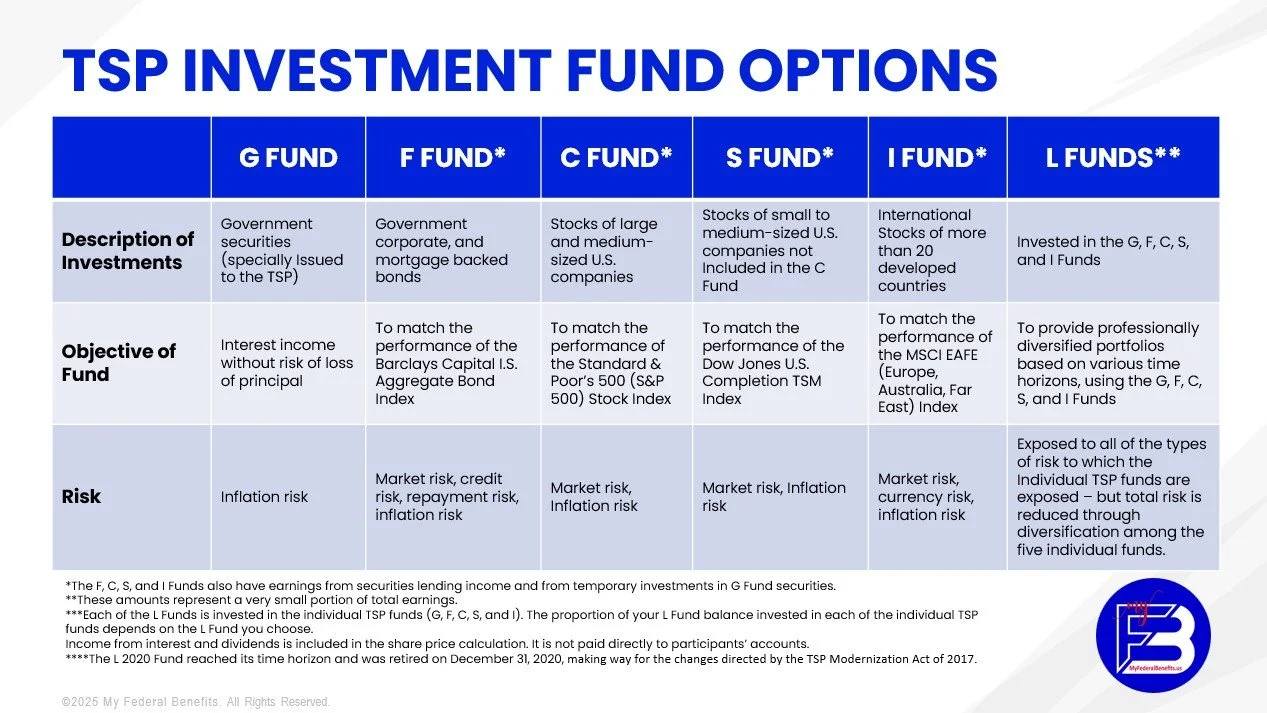

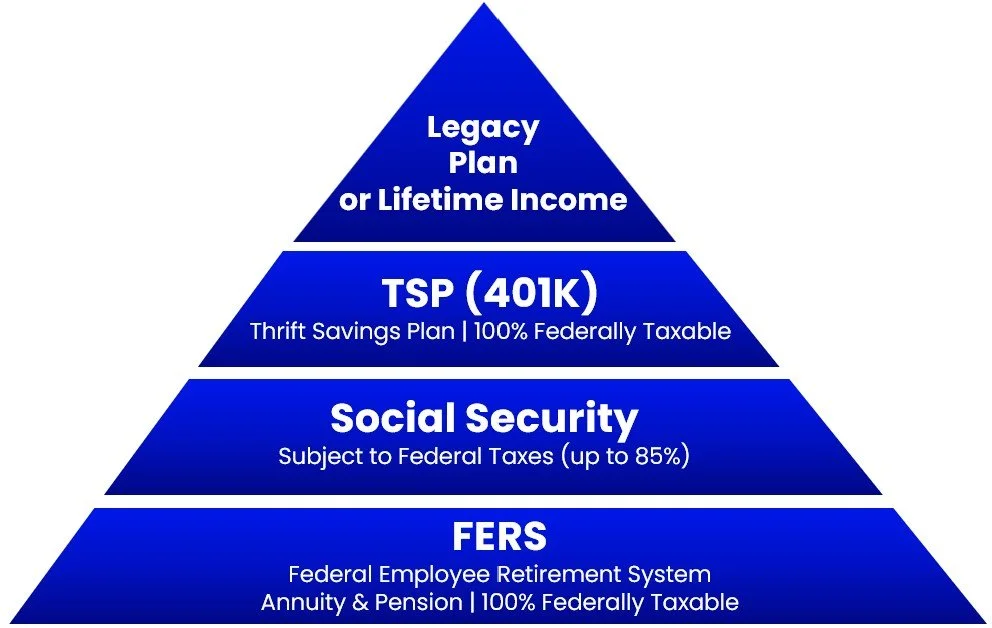

For years, the Thrift Savings Plan (TSP), the federal government’s retirement savings program , has served as a stable, low-cost way for federal employees to prepare for retirement. In 2026, however, changes are set to take effect. These include higher contribution limits and new Roth-related requirements, which could significantly alter how federal workers approach saving, tax planning, and future retirement withdrawals. While these changes appear incremental at first glance, it’s crucial that federal workers fully understand the details before making any adjustments to their existing retirement strategies.

Starting this year, federal employees can contribute up to $24,500 to their TSP, a $1,000 increase from years prior. Employees who are at least 50 will still be able to contribute an additional $8,000 in catch-up contributions. However, provisions in the SECURE 2.0 act are changing the way those catch-up contributions are taxed for certain employees. Beginning in 2026,federal workers who made more than $150,000 in 2025, any extra contributions must go into the Roth portion of your plan, meaning those dollars will be taxed upfront rather than deferred.

For federal workers who are early in their careers, higher contribution limits may not feel urgent. But over time, even small contribution increases can significantly affect your retirement lifestyle. While federal agencies automatically contribute 1% of pay regardless of participation, contributing at least 5% allows employees to receive the full government match, essentially doubling their savings. If employees continue making consistent contributions that are close to the maximum over a 30-year period, they could save more than $1 million in principal alone. For younger employees, time is the most powerful asset. But for those nearing retirement, the strategy shifts from long-term compounding to maximizing how much can be saved during the final working years.

By maximizing the current contribution limit, an employee planning to retire within the next five years could contribute roughly $122,500 in new savings, before factoring in any investment growth. Once catch-up contributions and agency matching are factored in, employees could contribute more than $30,000 per year. Even over a relatively short window, that level of disciplined saving — combined with modest growth — can meaningfully strengthen a retiree’s financial stability.

While contribution levels determine how much is saved, determining how many dollars retirees will actually keep depends on how they’re taxed. While traditional TSP contributions may reduce taxable income now, those dollars will be taxed as ordinary income once they’re withdrawn. Roth contributions, by contrast, are taxed up front and can be withdrawn tax-free in retirement. It is important to remember that contribution limits are the same whether dollars are directed to the Traditional or Roth portion of the plan.

Deciding whether to prioritize Traditional or Roth contributions shouldn’t be a one-size-its-all decision. It requires thoughtful consideration of current income, expected future tax brackets, retirement timelines, and overall financial goals.

With a in-plan Roth conversion, employees have the option to transfer funds from the Traditional portion of their TSP into the Roth portion. It will be taxed in the year it was converted. Employees should be mindful of how much they are converting in a single year because converting too much could push them into a higher tax bracket. On the other hand, because Roth balances are not subject to Required Minimum Distributions, strategic conversions may help reduce future mandatory withdrawals and provide greater long-term flexibility.

Beyond contribution strategy, federal workers should also think carefully about how retirement funds will eventually be withdrawn. Taking funds from Traditional accounts will increase taxable income while Roth withdrawals offer tax-free flexibility. Therefore, retirees who have Traditional and Roth balances can manage taxable income by coordinating withdrawals. For added flexibility and investment choice, some federal workers may also consider rolling assets into an IRA once they’ve retired.

While this year’s changes may seem technical, federal employees actually have a meaningful opportunity to be more intentional about retirement planning. The difference between a comfortable retirement and a strained retirement often comes down to the decisions made during working years. Rather than staying on savings-autopilot, consider reviewing how your contributions, tax positioning, and future withdrawal plans fit together. The coordination of those decisions can influence not only how much you are able to save, but how much you ultimately keep.

Taking the time to run the numbers, ask questions, and refine your approach today can lead to greater flexibility, stability, and confidence when retirement arrives.

2026 TSP Updates Could Change Retirement Strategies: What Federal Employees Need to Know

Eric M. Steffy is the Founder and CEO of Federal Solutions Support, and a Senior Federal Benefits Expert with more than 38 years of experience helping federal employees navigate retirement. Known for his high-integrity approach and deep expertise in federal and state benefits systems, Eric is dedicated to ensuring clients are well-positioned to maximize their retirement income and benefits.

When it comes to Federal benefits, experience matters.

Trust the experts - it’s been our specialty for 38 years.