Federal Solutions

Social Security 2026

As featured on ABC, CBS, NBC, & FOX TV, U.S. News & World Report, GoBankingRates, yahoo!finance,

AOL Finance, MSN money, Nasdaq Personal Finance & more.

Contributing to the National Conversation

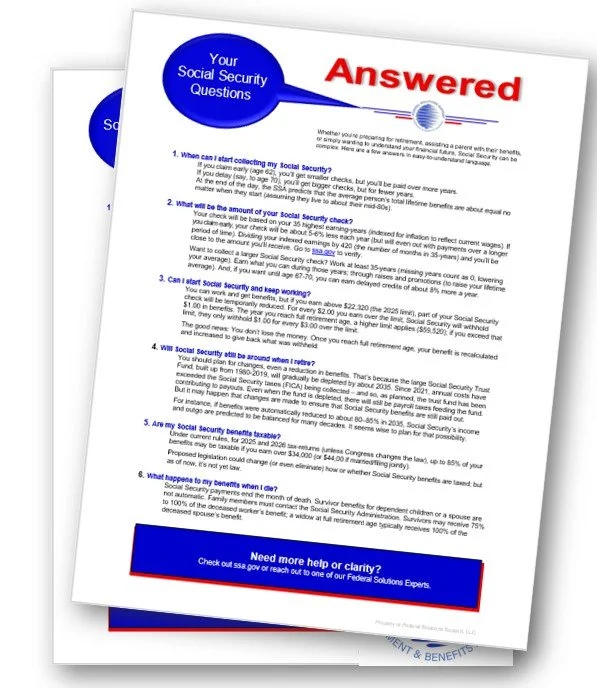

Many people miss out on maximizing their Social Security earnings, because they believe they will earn more if they delay the moment when they begin collecting their benefit.

While it’s true that your Social Security benefit will increase (up until age 70) if you wait until your older to begin collecting your Social Security benefits – the total amount received is often lower than if you had begun taking Social Security earlier.

Many people don’t know that the Social Security Administration has actually budgeted the same amount for you; whether you choose to take your payments early or later.

While taking Social Security as early as age 62 (for those without a disability) can lower your monthly check as much as 30%, here’s the kicker – you won’t necessarily earn less money by collecting Social Security before your full retirement age.

Taking Social Security earlier means that you’ll get a smaller monthly check. But you’ll receive payments over more years than someone who waited.

If you wait to collect Social Security and collect a larger check, but only happen to get that check for a few years (due to lifespan), you’ll receive a much lower amount than if you had started collecting earlier.

In theory, whether your take your Social Security benefits earlier or later – at the end of the day – you will earn the same amount (if you live into your late 70’s); statistically speaking.

In fact, if you calculate that the total benefits received by claiming early, you’ll discover that claiming early could be beneficial.

If your full retirement age is 67, and at that age you’d receive $2,000/month, but you decide to retire when you’re 63, your benefit will be reduced by 25. You’ll get a smaller check of only $1,500/month; with annual Social Security payments totaling $18,000. Between age 63 to age 73 you’ll earn a total of $180,000.

You’ll hear a lot of fear-tactics around how much you’ll lose annually – it’s not insignificant at $6,000 less a year, with a 10-year loss of $60,000.

However, by age 83 you would have earned = $360,000. That’s $48,000 more than if you lived to 83 and had delayed taking your social security until Full Retirement Age (67).

If you wait until full retirement age (67) in order to collect your full $2000 monthly payment, by age 73 you would have earned $24,000 a year.

Between age 63 to age 73, you will have earned $144,000, and by age 83 you would have earned $312,000. That’s $48,000 less (using this example) than those who began taking their Social Security at age 63.

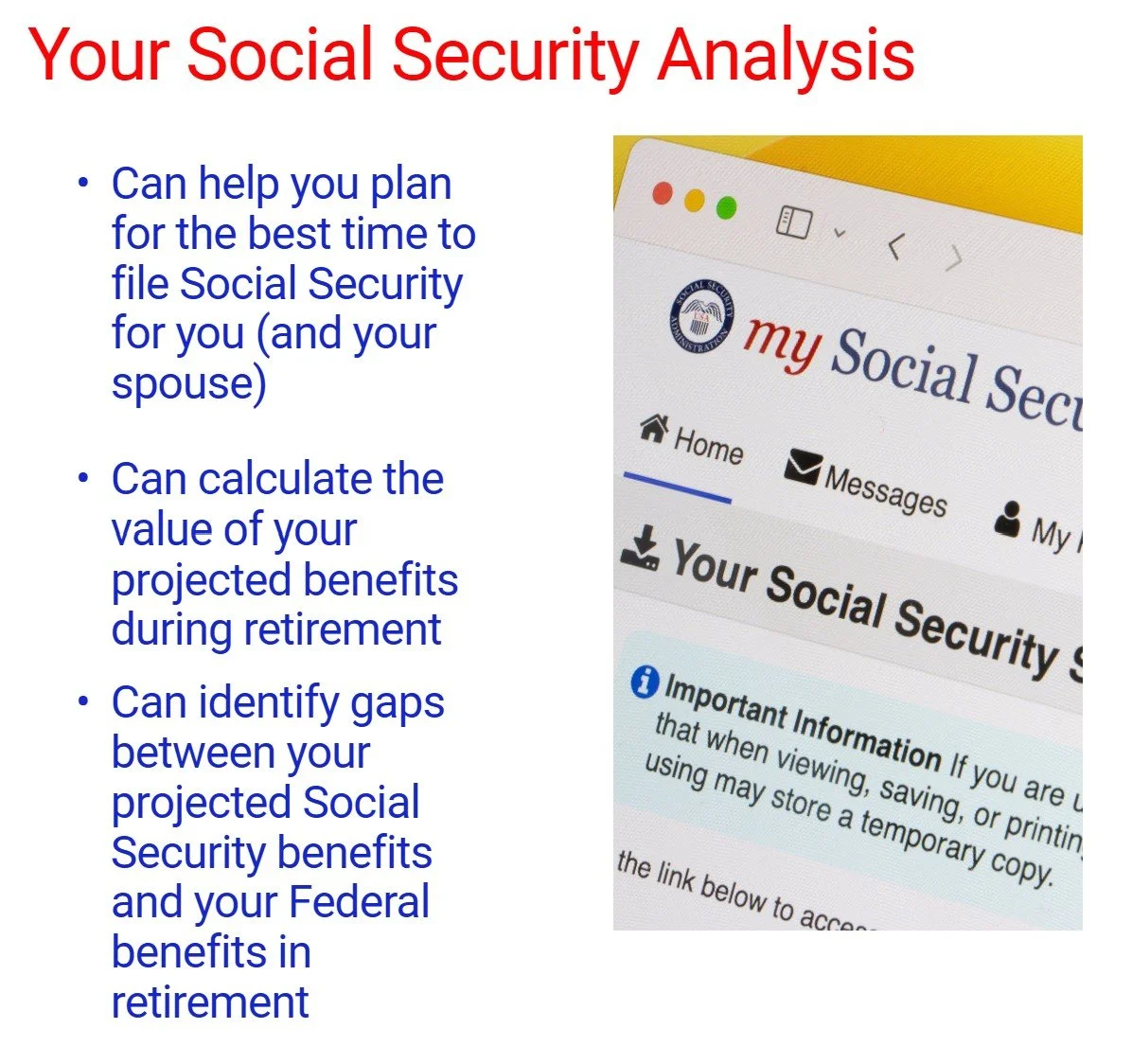

Knowing when to start taking your Social Security Benefits can be confusing.

Waiting works, especially if you still need to or want to work; as earning more than $22,320 a year will reduce your benefits $1 for every $2 you earn (until you’ve reached full retirement age, or about 67-years of age).

But, if you need the money now, start collecting your Social Security now. The payment will be lower than if you waited a few more years, but if you’re fortunate enough to collect your Social Security for 20-years, you will have earned more than if you’d waited.

For instance, if you wait until your 70-years old, and live for another decade (age 80), you will have collected less than half of those who began collected at 62 and lived to 80.

Your Social Security payment will be based on your 35 highest-earning years.

If you had a few years off in the middle of your earning career and can close the gap on that 35-total-years, it can be worth it to remove a few zeros from your overall average.

One of the other things we find that clients may have overlooked, is the ability to collect spousal or survivor benefits, and the calculations needed to ensure that you’re collecting the larger portion.

If you’re 62 or older, were married for 10 or more consecutive years and are currently unmarried (or remarried at age 62 or older), have been divorced for two or more years, and your former spouse is 62 or older – you can receive a benefit based on the earnings of your ex-spouse.

There are a lot of “if’s” there, so call the Social Security Administration or talk with a Federal Benefits Expert to get clarity on whether you’d be better off claiming your Social Security, or claiming spousal or survivor benefits.

Another big ‘oops’ we see people make, is earning too much once they start collecting Social Security.

If you still need to or want to work, earning more than $22,320 a year will reduce your benefits $1 for every $2 you earn; until you’ve reached full retirement age, at about 67-years for most individuals.

If you don’t know where to start, a Federal Solutions Expert can assist you with creating or assessing your overall retirement plan. They can also help you identify and implement appropriate Social Security strategies.

There are several situations where taking Social Security benefits earlier (before full retirement age) makes sense.

If you have a family health history that concerns you, consider collecting Social Security earlier – allowing you to receive payments for a longer period of time.

Conversely, if you think you’ll beat the average life expectancy – used by Social Security (84 for men, 87 for women) – then, if you can afford it, it might pay to wait as you could possibly collect a larger payment for more than the 20-years that Social Security estimates they will pay you.

Also, if you currently have a health or financial need, please don’t wait to collect your Social Security now.

If your savings or pension aren’t enough to cover your essential expenses, and Social Security can you help you make ends meet – please don’t wait to begin collecting your benefit.

If you lose your job or retire early – something many Federal Employees are currently facing – and you need income before you reach full retirement age, early Social Security benefits can help bridge the gap.

If delaying Social Security means withdrawing from investments that are performing well or are subject to market volatility, taking benefits earlier may help preserve your portfolio.

If you’re married and your Social Security will be less than your spouse’s, another way to hedge your bets is to start collecting yours now – and let your spouse’s earn the 8% credit that begins at post-retirement-age.

Some retirees prefer to claim benefits early to fund travel, hobbies, or experiences while they are still healthy enough to enjoy them.

Experts like Federal Solutions help federal employees make sure they’re in a strong position that can last a lifetime. Don’t guess. Get help making sure your finances are working for you.

Receiving funds from the Social Security Fairness Act

For some people that means that you’ll now receive a one-time payment (sometimes as much as $6,000), for others it may mean receiving an increased monthly payment.

Receiving an unbudgeted windfall may tempt you to make a few things on your wish-list come true; that dream trip, auto, or other purchase.

It’s absolutely fun to go for that wish list. But, it may be even more satisfying to erase stress by reducing debt. Debt stress actually takes a toll on physical and emotional health.

If you’re one of those lucky enough to be receiving funds from the Social Security Fairness Act, it’s because you were unlucky earlier and went without some of the social security benefits seen by your peers.

Retirees who qualify for retroactive payments may receive a lump sum payment of as much as $6,000. While it’s tempting to spend that on your one big wish (a new toy, a trip, home improvement) – putting $6,000 toward the principal of a loan can reduce your monthly payments or even shorten your loan duration. And, that can save you money which, down the road, you can spend on that wish-list!

For instance, if you have a home mortgage with 10-years remaining on your mortgage and you owe $100,000, then a $6,000 payment now (all of your Social Security retroactive payment) could mean that your loan will be paid off one year earlier. And, if you also added any monthly increase in social security disbursements directly to your mortgage payment (say, $150/month), you’ll pay your loan off as much as 3-years earlier; saving yourself as much as 17% on interest. You can apply a similar savings formula to paying off credit card or auto debt.

Paying down debt turns that added Social Security payment into even more money for you, buy eliminating the interest you would otherwise owe.

Choosing which debt to payoff first is often part math and part how we feel about that debt.

Prioritizing high-interest debt will save you the most money. If all of your debt interest-rates are similar, choosing which debt to lift off your shoulders may come down to what makes you feel safest as you head into the future. For some people, that means tackling mortgage debt, ensuring there is less risk to the roof over their head. For others, it may mean adding to a fixed annuity, with guaranteed income for life.

Experts like Federal Solutions helps federal employees make sure they’re in a strong position that can last a lifetime. Don’t guess. Get help making sure your finances are working for you.

In earlier times, a lot of people retired and slowed down.

But today’s retirees are pursuing the dreams with a passion. And that has created a new phenomenon. Debt load has quadrupled for today’s seniors between age 65 and 74. And, that can change a stress-free retirement into one fraught with financial anxiety. If you’re receiving funds from the Social Security Fairness act, this is your moment to decrease your debt, lower your overall stress, and buy yourself a little peace of mind.

Ideally, your emergency fund should have at least $10,000 in it, though some people are able to ensure they have an even larger cushion. My guess is, if you’re cringing at the thought of not having the emergency reserves you may need, you’ll feel a huge relief by using your additional Social Security funds to invest in you, in your security and peace of mind. Make that emergency fund a reality.

If you’ve received (or expect to receive) funds from the Social Security Fairness Act, the second thing to spend your money on (instead of your wish-list) is to consider making a dent in any debt that’s hanging over you.

Redirecting that Social Security windfall to eliminating debt – is an investment in your well-being.

We don’t talk about it, because it makes people feel uncomfortable. But, the reality is that three out of every four adults, over the age of 50, is carrying significant debt. And, making debt payments once you’re on a fixed, retirement-income can feel exhausting.

For most retirees, carrying a mortgage, car loan, or credit card debt – while also paying for food, health care, and often contributing to the support of others – can create a sense of vulnerability.

So, it’s worth considering whether you could use some, or all, of the funds you receive from the Social Security Fairness Act to buy your way out of the stress that comes from carrying debt.

We need to look at paying down debt, not as depriving ourselves of something we really want, but as an investment in our peace of mind. In this case, you can actually buy health. Less debt can lower your stress level by 50%, reduce relational conflict, and contribute to your overall well-being.

The first thing you should do with any influx of funds you receive from the Social Security Fairness Act, is create or contribute to an emergency fund.

Life happens. And, having an emergency fund, for a time when you’ll face unexpected costs, can keep you from running up high-interest charges on a credit card, taking high interest loans, or dipping into accounts budgeted for daily expenses.

Having an emergency fund is a critical step for ensuring financial stability and providing a safety net during unexpected events. For seniors, the number one big-ticket expense is unexpected dental bills, because most costly dental procedures aren’t covered by Medicare. The second largest unexpected financial event is changes in housing costs or property assessments.